Fintech vs Traditional Banking, Pakistan stands at a pivotal moment in its economic development, with two distinct financial pathways unfolding simultaneously. On one side, traditional banking institutions with their established branch networks and decades of customer relationships continue to dominate the financial landscape. On the other, agile fintech startups are rapidly transforming how Pakistanis save, spend, and access financial services.

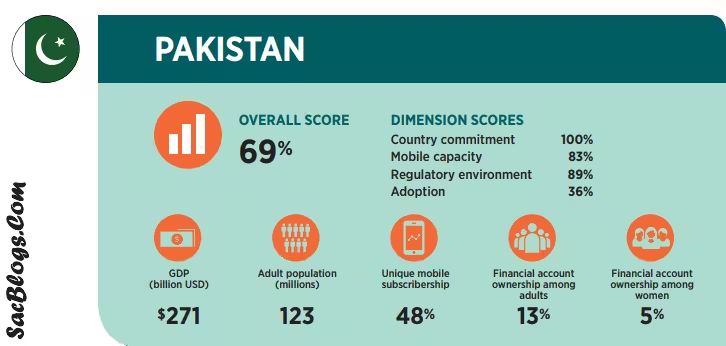

With a population of 240.5 million and ambitious government targets to increase adult financial inclusion from 64% to 75% by 2028, the competition between these models has never been more consequential . This digital transformation is occurring against a backdrop of massive technological adoption 143 million broadband subscribers and 193 million cellular connections create fertile ground for financial innovation .

As we examine the relative strengths and challenges of both fintech and traditional banking, a crucial question emerges: which approach better serves Pakistan’s future? The answer, as we’ll discover, may lie not in choosing one over the other, but in harnessing the unique advantages of both.

Table of Contents

The Rise of Fintech in Pakistan: Democratizing Financial Access

Understanding the Fintech Phenomenon

Fintech, the fusion of finance and technology, represents a fundamental reimagining of how financial services can be delivered and experienced . In Pakistan, this sector has evolved from simple digital payment platforms to a comprehensive ecosystem encompassing lending, wealth management, remittances, and insurance. What distinguishes fintech companies is their singular focus on leveraging technology to create more accessible, efficient, and user-friendly financial solutions. Without the physical infrastructure and legacy systems that constrain traditional banks, fintechs have demonstrated remarkable agility in addressing gaps in Pakistan’s financial landscape.

Driving Forces Behind Fintech Adoption

Several powerful trends converge to accelerate fintech adoption across Pakistan. The country’s young, tech-savvy population shows increasing preference for digital-first solutions that offer convenience and speed. Regulatory initiatives from the State Bank of Pakistan (SBP), including frameworks for Electronic Money Institutions (EMIs) and the launch of Raast—an instant payment system have created a more supportive environment for innovation . The significant penetration of mobile devices provides the essential infrastructure for digital financial services to reach even remote populations. Additionally, the COVID-19 pandemic acted as an unexpected catalyst, accelerating digital adoption as consumers sought contactless financial solutions during lockdowns .

Fintech’s Strategic Advantages

- Financial Inclusion: Digital wallets and branchless banking models extend financial access to populations traditionally excluded from formal banking . With over 50% of Pakistan’s adult population remaining unbanked, this represents a massive opportunity for growth and inclusion .

- User Experience: Fintech platforms prioritize intuitive, app-based interfaces that simplify financial transactions. This user-centric design philosophy stands in stark contrast to the often cumbersome processes associated with traditional banking.

- Innovation Speed: Unencumbered by legacy systems and bureaucratic hurdles, fintech companies can rapidly develop and deploy new features in response to market demands.

- Cost Efficiency: Without the overhead of maintaining physical branches, fintechs can operate with significantly lower costs, potentially passing these savings to consumers through reduced fees .

Traditional Banking’s Enduring Strengths: Stability in a Changing Landscape

The Bedrock of Pakistan’s Financial System

Traditional banks have long formed the foundation of Pakistan’s financial infrastructure, with institutions like HBL, UBL, Meezan Bank, and Bank Alfalah maintaining extensive branch networks across the country . These establishments provide comprehensive financial services encompassing savings and checking accounts, personal and business loans, trade finance, and insurance products. Despite the rapid growth of digital alternatives, traditional banks continue to command significant market share, with the traditional banking sector projected to reach a net interest income of US$6.29 billion by 2025 .

Institutional Strengths and Advantages

- Trust and Security: Traditional banks benefit from longstanding reputations and are generally perceived as more secure and reliable by consumers . The presence of physical branches provides tangible reassurance, particularly for customers less comfortable with digital-only platforms.

- Comprehensive Service Offerings: Unlike many fintechs that specialize in specific product verticals, traditional banks provide integrated financial solutions ranging from basic accounts to complex corporate banking products .

- Regulatory Framework: Operating within well-established regulatory parameters provides traditional banks with clearly defined operational boundaries and oversight mechanisms.

- Established Customer Relationships: Decades of service have allowed traditional banks to develop deep relationships with both individual and corporate clients, creating stickiness that pure digital players struggle to replicate.

Adaptation and Digital Transformation

Facing increasing competition from fintech startups, traditional banks have embarked on their own digital transformation journeys. Many have developed mobile banking applications, online portals, and implemented technologies like AI and blockchain to enhance operational efficiency and customer experience . This hybrid approach combining digital convenience with physical presence represents a strategic response to the fintech challenge. According to recent research, this digital transformation, while creating upfront costs, ultimately contributes to greater financial stability by increasing Z-scores and lowering non-performing loan ratios .

Comparative Analysis: Fintech vs Traditional Banking Across Critical Dimensions

| Aspect | Fintech | Traditional Banks |

|---|---|---|

| Regulatory Body | SECP (for NBFCs), State Bank of Pakistan (for digital banks, EMIs) | State Bank of Pakistan |

| Reach & Accessibility | Primarily urban and digitally-savvy users, but expanding to underserved areas via mobile access | Wide national reach, especially in urban and semi-urban areas |

| Innovation Speed | Fast-paced, tech-forward, agile development | Slower innovation due to regulations and bureaucratic processes |

| Product Range | Specialized: payments, lending, remittances, wallets | Comprehensive: loans, savings, trade finance, insurance |

| User Experience | App-based, user-friendly, digital-first design | Improving but often traditional and paper-heavy processes |

| Trust & Security | Gaining ground but still building consumer trust | Long-standing reputation, generally seen as more secure and reliable |

| Cost Structure | Lower overhead, lean operations | Higher overhead due to physical infrastructure and legacy systems |

| Financial Inclusion | Targeting underserved/unbanked populations via mobile access | Expanding inclusion but facing infrastructure limitations in rural areas |

Sector-Specific Impact and Market Outlook

Digital Payments Revolution

The digital payments sector represents one of fintech’s most significant inroads in Pakistan. Platforms like JazzCash and Easypaisa have revolutionized money transfers, bill payments, and mobile top-ups, with each boasting over 15 million users . These platforms have become particularly impactful for populations with limited access to traditional banking services. The SBP projects Pakistan’s digital payments sector to reach $36 billion by 2025, indicating substantial growth potential .

Lending and Credit Innovation

Fintech companies are transforming credit accessibility through alternative lending models. Startups like Credit Book provide micro-loans to SMEs and individuals often excluded from traditional banking services . By leveraging non-traditional data sources and advanced algorithms, these platforms can assess creditworthiness for segments of the population that lack conventional credit histories.

The Remittances Opportunity

For a country where remittances play a vital role in the economy, fintech platforms are streamlining international money transfers. Companies like SadaPay are digitizing these processes, reducing costs and transfer times for the Pakistani diaspora sending money home . This digital transformation has significant implications for financial inflows that support millions of households.

Market Size and Growth Trajectory

The digital banking sector is expected to reach US$309.84 million in net interest income by 2025, with an annual growth rate (CAGR 2025-2030) of 3.09%, projected to reach US$360.76 million by 2030 . While still modest compared to the traditional banking sector’s projected US$6.29 billion in net interest income for 2025 , the growth rates indicate a gradual market shift toward digital solutions.

Challenges and Constraints: Navigating the Road Ahead

Fintech Growing Pains

Despite their rapid growth, Pakistani fintech companies face significant challenges. Regulatory hurdles present ongoing obstacles, with evolving frameworks sometimes struggling to keep pace with innovation . Limited financial literacy among segments of the population hampers broader adoption of digital services . As digital transactions increase, cybersecurity risks become more pronounced, requiring robust security measures . Perhaps most critically, attracting venture capital remains a challenge compared to regional peers, potentially limiting scaling opportunities .

Traditional Banking Transformation Challenges

Traditional institutions face their own set of challenges in adapting to the new financial landscape. Many struggle with legacy systems that impede digital integration and increase transformation costs . The cultural shift from traditional to digital operations requires significant organizational change. Established banks must balance innovation with stringent regulatory compliance requirements . Additionally, these institutions face increasing competition not only from fintech startups but also from digital banks that offer modern user experiences without the overhead of physical branches .

The Trust Paradox

A fundamental challenge across both sectors revolves around trust. While traditional banks benefit from established reputations, they must overcome perceptions of being outdated or bureaucratic . Fintech companies, though perceived as modern and convenient, must build consumer confidence in their security and long-term viability . This trust building is particularly crucial in rural areas where populations may be more cautious about digital financial services.

The Path Forward: Collaboration as the Key to Pakistan’s Financial Future

Emerging Hybrid Models

Rather than an either-or proposition, the most likely outcome for Pakistan’s financial future involves strategic collaboration between fintech innovation and traditional banking stability. We already see promising examples of this synergy: traditional banks partnering with fintech companies to offer enhanced digital services, fintechs leveraging banking infrastructure to expand their reach, and hybrid products that combine the strengths of both models . These collaborations create powerful synergies—fintechs gain access to established customer bases and regulatory expertise, while banks infusion innovation and digital capabilities.

The Evolving Regulatory Landscape

The State Bank of Pakistan plays a crucial role in shaping this collaborative future through balanced regulation that encourages innovation while ensuring financial stability. The SBP’s regulatory frameworks for Electronic Money Institutions and the Raast instant payment system demonstrate this balanced approach . As the financial landscape evolves, regulatory flexibility will be essential to accommodate new business models while protecting consumers and maintaining systemic stability.

Regional Context and Global Perspective

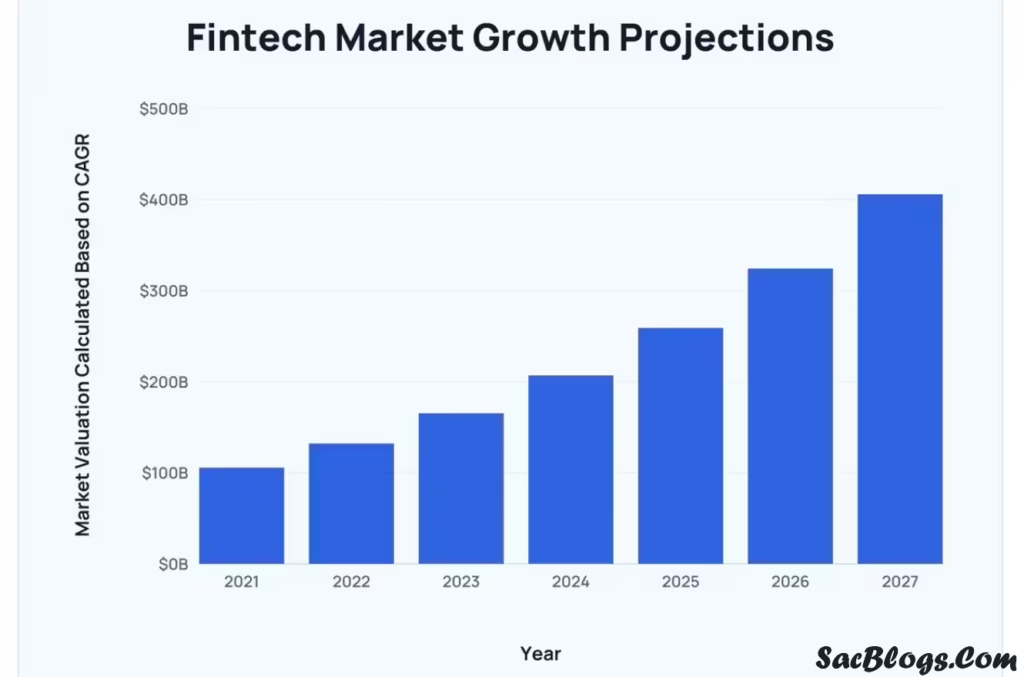

Pakistan’s fintech evolution occurs within a broader regional context, with India’s exponential fintech growth serving as both inspiration and benchmark . Pakistan’s Raast system draws inspiration from India’s highly successful UPI platform . Globally, while fintech investment saw a 20% decline to $43 billion in 2024, the sector remained the top-funded across emerging venture markets, indicating sustained investor confidence despite macroeconomic challenges .

Conclusion: A Complementary Future for Pakistani Finance

As Pakistan stands at this financial crossroads, the evidence suggests that the nation doesn’t need to choose between fintech and traditional banking, but rather embrace a future where both coexist and complement each other. Each brings distinct strengths to the table—fintech offers innovation, accessibility, and user-centric design, while traditional banks provide stability, comprehensive services, and established trust. For consumers, this means increasingly diverse options tailored to different needs and preferences.

For Pakistan’s economic future, this synergistic approach promises accelerated progress toward financial inclusion goals, enhanced efficiency in financial intermediation, and greater resilience in the face of economic challenges. The ultimate beneficiaries will be Pakistani consumers and businesses, who will enjoy unprecedented choice, accessibility, and convenience in managing their financial lives.

The transformation ahead will require continued regulatory foresight, strategic investments in digital infrastructure, and commitment to financial literacy. By harnessing the innovative potential of fintech while preserving the stabilizing influence of traditional banking, Pakistan can build a financial ecosystem that drives inclusive growth and positions the nation for prosperity in the digital age.

Read Also:

- Fintech Startups and the Road to a Digital Pakistan 2026 – A Comprehensive Analysis

- How Mobile Banking and Fintech Are Empowering the Unbanked in Pakistan for 2026

- Why Cashless Payments Are the Future of Business in Pakistan in 2026

FAQs: Fintech vs Traditional Banking in Pakistan

1. How does fintech promote financial inclusion in Pakistan?

Fintech companies expand financial access through mobile-based solutions that don’t require physical branches, digital wallets that need minimal documentation, and alternative credit scoring methods that serve those without traditional banking histories . This is particularly crucial in a country where over 50% of adults remain unbanked.

2. Are traditional banks in Pakistan becoming obsolete?

No, traditional banks are not becoming obsolete. While they’re experiencing gradual market share erosion, they still dominate the financial landscape with projected net interest income of US$6.29 billion by 2025 . Traditional banks are adapting by investing in digital transformation and often partnering with fintech companies .

3. Which is more secure: fintech apps or traditional banks?

Traditional banks currently maintain an advantage in perceived security due to their long-standing reputations and physical presence . However, fintech companies are rapidly enhancing their security measures and building consumer trust as the market matures.

4. How is the State Bank of Pakistan regulating fintech?

The SBP has established frameworks for Electronic Money Institutions (EMIs), launched the Raast instant payment system, and created a regulatory environment that balances innovation with financial stability . The SECP also regulates non-banking financial companies in the fintech space .

5. Can Islamic banking coexist with fintech innovation?

Yes, Islamic banking and fintech can not only coexist but complement each other. Research shows that while Islamic banks may adopt fintech more slowly due to Shariah compliance requirements, they potentially gain significant stability benefits from digital transformation .

6. What are the main challenges for fintech growth in Pakistan?

Key challenges include regulatory complexity, limited financial literacy in certain segments, cybersecurity concerns, and difficulties in attracting venture capital compared to regional peers .

7. How does Pakistan’s fintech landscape compare regionally?

Pakistan’s fintech evolution is inspired by regional successes like India’s UPI system . While still developing, Pakistan shows significant potential with its large youth population, growing mobile penetration, and regulatory initiatives supporting digital finance.

8. Which sectors within fintech are seeing the most growth in Pakistan?

Digital payments lead fintech growth, followed by lending and credit innovations, remittance platforms, and emerging wealth management solutions . Digital banks are also experiencing rapid growth, projected to reach US$309.84 million in net interest income by 2025 .

9. How does fintech impact banking stability in Pakistan?

Research indicates that proper fintech adoption can enhance bank stability by improving risk management capabilities, though it may initially increase operational costs before efficiency gains are realized .

10. What role does AI play in Pakistan’s banking transformation?

Artificial intelligence is increasingly being deployed for credit scoring, customer service through chatbots, fraud detection, and personalized banking experiences, with both traditional banks and fintech companies leveraging these technologies .

1 thought on “Fintech vs Traditional Banking – Which Will Shape Pakistan’s Financial Future in 2026”