In 2026, digital wallets are fundamentally reshaping Pakistan’s economic landscape, serving as a powerful catalyst for financial inclusion and economic modernization. From remote villages to urban centers, platforms like JazzCash, EasyPaisa, and emerging digital banks are transforming how Pakistanis save, spend, and build economic security. This transformation is accelerating Pakistan’s journey toward a cashless economy, driven by strategic government initiatives, rapidly evolving financial technology, and a young, tech-savvy population.

The integration of digital wallets into everyday commerce and government services is not merely a convenience but a fundamental rewiring of the nation’s economic infrastructure, creating new pathways for growth and inclusion across all segments of society. As we explore the multifaceted impact of this digital revolution, it becomes clear that digital wallets are becoming the indispensable engine of Pakistan’s economic future, connecting millions to the formal economy for the first time and building a more resilient, transparent, and inclusive financial ecosystem for all citizens.

Table of Contents

The Current Landscape: Digital Wallets in Pakistan

Pakistan’s digital wallet ecosystem has evolved from simple money transfer services to comprehensive financial platforms. Since the 2009 launch of EasyPaisa, the market has expanded to include players like JazzCash, Nayapay, and SadaPay, which offer increasingly sophisticated services including international payments, bill settlements, and access to credit . This evolution has positioned digital wallets as critical infrastructure within Pakistan’s broader Digital Public Infrastructure (DPI), working in tandem with national identity systems managed by NADRA to verify identities and streamline the onboarding of new users .

The rapid adoption of these platforms is reflected in transaction volumes. Digital transaction values in Pakistan surged by 35% in recent years, with mobile devices accounting for 80% of e-commerce volume . This growth trajectory aligns with global trends, where the value of digital wallet transactions is projected to exceed $12 trillion by 2026 . Underpinning this expansion is a robust regulatory framework developed by the State Bank of Pakistan (SBP), which has established regulations for Electronic Money Institutions (EMIs) and a Regulatory Sandbox to foster innovation while ensuring security and consumer protection .

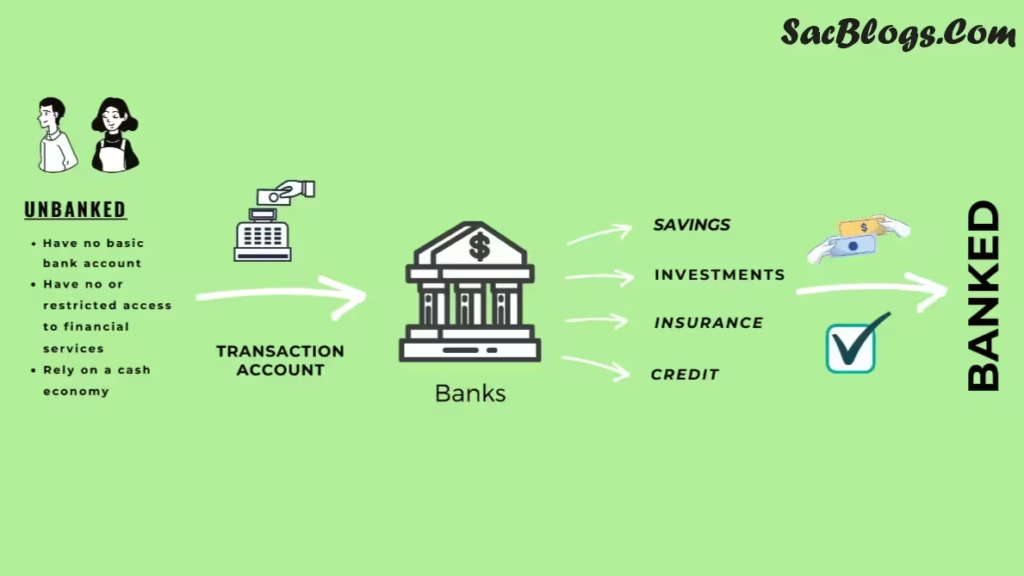

Driving Financial Inclusion: Reaching the Unbanked Masses

Perhaps the most transformative impact of digital wallets on Pakistan’s economy lies in their unprecedented ability to advance financial inclusion. By eliminating the need for physical bank branches and extensive paperwork, digital wallets have dramatically reduced barriers to financial access, particularly for marginalized communities .

Empowering Women Economically

Digital wallets are playing a crucial role in narrowing the financial gender gap in Pakistan, where only 13% of women previously had personal bank accounts compared to 28% of men . By providing women with direct control over financial resources, these platforms offer increased autonomy and security. Evidence shows that when women receive payments directly into their digital wallets, they maintain significant control over spending decisions—with one study showing 91% of women maintaining complete control over how aid money was spent . This financial empowerment is particularly significant in a patriarchal context, helping to mitigate traditional barriers such as limited mobility and spousal control over cash resources .

Serving Rural and Underserved Communities

For Pakistan’s rural populations, digital wallets have become a gateway to the formal economy. Platforms like JazzCash and EasyPaisa have built extensive agent networks that allow users in areas with limited banking infrastructure to convert cash to digital value and access essential financial services . This infrastructure has proven particularly valuable for humanitarian aid distribution, where research has shown that digital delivery reduces collection time by 7% and transportation costs by 20% compared to traditional cash distribution methods . Even among populations with minimal prior exposure to technology—including where 84% had no formal education—digital wallets have demonstrated remarkable accessibility, with over 99% of recipients successfully accessing their funds .

Fueling Economic Growth: The Macroeconomic Impact

The widespread adoption of digital wallets is generating substantial macroeconomic benefits for Pakistan, contributing to economic formalization, efficiency gains, and the growth of digital commerce.

Formalizing the Economy and Enhancing Transparency

Digital wallets are playing a crucial role in bringing millions of Pakistan’s informal economic participants into the formal financial system. As Finance Minister Muhammad Aurangzeb noted, digital banking platforms significantly contribute to “documenting the informal economy by bringing millions of unbanked citizens into the formal financial sector” . This transition expands the tax base, improves economic measurement, and enhances policy effectiveness. The inherent transparency of digital transactions also helps reduce corruption and “leakage” in government transfer programs, ensuring that resources reach their intended beneficiaries .

Catalyzing E-commerce and Entrepreneurial Activity

The growth of Pakistan’s e-commerce sector—projected to reach US$12 billion by 2027—is inextricably linked to the expansion of digital payment systems . Digital wallets provide the essential payment infrastructure that enables online commerce, particularly in a context where cash-on-delivery previously dominated. For entrepreneurs and small businesses, digital wallets facilitate access to broader customer bases, streamline business operations, and create opportunities to establish credit histories based on transaction data . The number of registered e-commerce merchants in Pakistan grew by 427% between 2019 and 2023, a expansion fueled by the availability of digital payment channels .

| Indicator | Recent Growth/Status |

|---|---|

| E-commerce Volume (2024) | US$7.7 billion |

| Projected E-commerce Volume (2027) | US$12 billion |

| Registered E-commerce Merchants (2019-2023) | 427% growth |

| Digital Transaction Volumes | 35% surge |

| ICT Exports | 25.5% surge over 8 months |

Government Initiatives and Digital Public Infrastructure

Pakistan’s transition to a digital economy is being accelerated through strategic government initiatives and substantial investments in Digital Public Infrastructure (DPI). These efforts are creating an ecosystem where digital wallets can thrive and reach their full potential.

Strategic Policy Frameworks

The Government of Pakistan has demonstrated strong commitment to digital transformation through several key initiatives:

- Digital Economy Enhancement Project (DEEP): This World Bank-funded project aims to strengthen Pakistan’s digital economy and identity systems by developing responsible data-sharing protocols, digital authentication systems, and verifiable credentials .

- Digital Foreign Direct Investment (DFDI) Initiative: Pakistan became the first country globally to introduce this initiative, positioning itself as a regional leader in digital transformation and attracting foreign investment into its digital ecosystem .

- Digital Pakistan Policy: This comprehensive policy provides a roadmap for digital transformation, emphasizing broadband expansion, enabling policies, and legal frameworks to support the digital economy .

Integration with National Digital Identity Systems

A critical factor in the success of digital wallets has been their integration with Pakistan’s national identity system managed by NADRA. This integration has streamlined identity verification processes, reduced fraud, and made it significantly easier for unbanked populations to access financial services . As Tariq Malik, former chairman of NADRA, explained: “Integration of NADRA’s biometric authentication with digital wallets can help to reduce fraud and increase system confidence” . This secure identity infrastructure forms the backbone of Pakistan’s evolving digital ecosystem, enabling trusted transactions between parties who may not have previous relationships.

The Future Outlook: Digital Wallets in 2026 and Beyond

As Pakistan continues its digital transformation journey, several trends are shaping the future trajectory of digital wallets and their role in the national economy.

Technological Advancements and Service Diversification

Leading digital wallet providers are increasingly diversifying their service offerings beyond basic payments to include new solutions such as buy-now-pay-later options, micro-investment products, and cryptocurrency transactions . This diversification mirrors global trends where digital wallet providers are adding value-added services like loyalty rewards and credit to diversify revenue streams . Technological integration with other emerging technologies, particularly blockchain for remittances and supply chain finance, represents another promising frontier for Pakistan’s fintech sector .

Addressing Challenges and Expanding Inclusion

Despite significant progress, challenges remain in achieving universal adoption of digital wallets. The digital divide between urban and rural areas, limited internet connectivity in remote regions, and cybersecurity concerns present ongoing hurdles . Perhaps most significantly, gender disparities in adoption persist, with women facing barriers including limited access to mobile phones, lower digital and financial literacy, and familial restrictions . Addressing these challenges requires coordinated efforts from both public and private sectors, including targeted digital literacy programs, gender-sensitive product design, and infrastructure development .

| Challenge | Current Status | Potential Solutions |

|---|---|---|

| Gender Gap in Adoption | Less than 28% of mobile wallets owned by women | Gender-targeted transfers, financial literacy programs, community-based initiatives |

| Digital Divide | Limited internet connectivity in rural areas | Infrastructure investment, offline functionality, agent network expansion |

| Data Privacy & Security | Personal Data Protection Bill not yet formalized | Enhanced regulatory frameworks, cybersecurity measures, consumer education |

| Financial & Digital Literacy | Women score lower on financial literacy (44) and digital literacy (38) indices | Tailored literacy programs, simplified interfaces, community training |

Conclusion: Toward an Inclusive Digital Economy

The transformation of Pakistan’s economy through digital wallets represents one of the most significant economic developments of the decade. By providing accessible, secure, and efficient financial services to millions previously excluded from the formal economy, digital wallets are not merely changing how transactions occur—they are reshaping economic opportunities, empowering marginalized communities, and building a more inclusive and resilient economic foundation for the nation. As Prime Minister Shehbaz Sharif emphasized, accelerating the transition to a digital economy is essential for enhancing efficiency and broadening financial inclusion across the country .

The journey toward a fully realized digital economy continues, with ongoing needs for infrastructure development, regulatory refinement, and targeted efforts to ensure that all Pakistanis can participate in and benefit from the digital transformation. However, the progress already achieved demonstrates the tremendous potential of digital wallets to drive economic growth, reduce poverty, and build a more prosperous and inclusive Pakistan by 2026 and beyond. Through continued collaboration between government agencies, financial institutions, technology providers, and communities, Pakistan is well-positioned to realize the full potential of its digital future.

Read Also :

- Top 10 Fintech Trends Driving the Cashless Revolution in Asia 2026

- The Cashless Revolution – How Fintech is Reshaping Everyday Life in Pakistan 2026

Frequently Asked Questions (FAQs)

1. What are the most popular digital wallets in Pakistan in 2026?

The digital wallet landscape in Pakistan is dominated by platforms like JazzCash, EasyPaisa, Nayapay, and SadaPay. New digital banks like Mashreq Digital Bank have also entered the market, offering additional options for consumers .

2. How secure are digital wallets for everyday transactions?

Digital wallets in Pakistan incorporate multiple security measures, including integration with NADRA’s biometric verification system, which helps reduce fraud and identity theft . The State Bank of Pakistan regulates these platforms, establishing security standards and compliance requirements to protect consumers .

3. Can digital wallets be used in rural areas with limited internet connectivity?

Yes, digital wallet providers have established extensive agent networks in rural areas where internet connectivity may be limited. These agents facilitate cash-in and cash-out transactions, ensuring accessibility even in regions with poor digital infrastructure .

4. How are digital wallets helping to empower women economically in Pakistan?

Digital wallets provide women with direct control over financial resources, reducing dependence on male relatives and increasing financial autonomy. Research shows that 91% of women maintaining complete control over spending decisions when using digital wallets .

5. What role is the government playing in promoting digital wallet adoption?

The government is actively promoting digital wallets through initiatives like the Digital Economy Enhancement Project (DEEP), the Digital Foreign Direct Investment (DFDI) Initiative, and integration with NADRA’s digital identity system .

6. Are there special features for freelancers and businesses using digital wallets?

Yes, platforms like SadaPay and Nayapay offer special features for freelancers and small businesses, including support for international payments through partnerships with global card networks like MasterCard and Visa .

7. What percentage of e-commerce transactions in Pakistan are conducted through digital wallets?

While cash-on-delivery remains popular for e-commerce transactions (70% of transactions), digital payment adoption is growing rapidly, with 80% of e-commerce volume coming from mobile devices .

8. How do digital wallets benefit humanitarian aid distribution in Pakistan?

Research shows that digital delivery of humanitarian aid increases food security 22% more than traditional cash transfers, reduces transportation costs by 20%, and cuts collection time by 7% .

9. What are the main obstacles to digital wallet adoption in Pakistan?

Key challenges include the digital divide between urban and rural areas, cultural preferences for cash, cybersecurity concerns, and gender disparities in access to mobile phones and digital literacy .

10. How are digital wallets contributing to Pakistan’s formal economy?

Digital wallets are bringing millions of unbanked citizens into the formal financial sector, helping to document the informal economy, expand the tax base, and create more transparent financial flows .

2 thoughts on “Digital Wallets in 2026 – The Engine of Pakistan’s Economic Transformation”