In Pakistan, mobile banking a profound financial transformation is underway. With over 100 million unbanked adults in a population of roughly 240 million, the challenge of financial exclusion is significant . However, the rapid adoption of mobile banking and fintech solutions is turning this challenge into an opportunity for economic empowerment.

By 2026, Pakistan is poised to see a dramatic shift in its financial landscape, driven by government digitalization mandates and innovative private-sector solutions. This article explores how technology is bridging the financial divide, bringing secure, affordable, and accessible financial services to millions of Pakistanis who have long been left outside the formal economy. The journey towards full financial inclusion is complex, but the progress made by 2026 will lay a robust foundation for a more inclusive and prosperous economic future for all.

Table of Contents

The Scale of the Challenge: Understanding Pakistan’s Unbanked Population

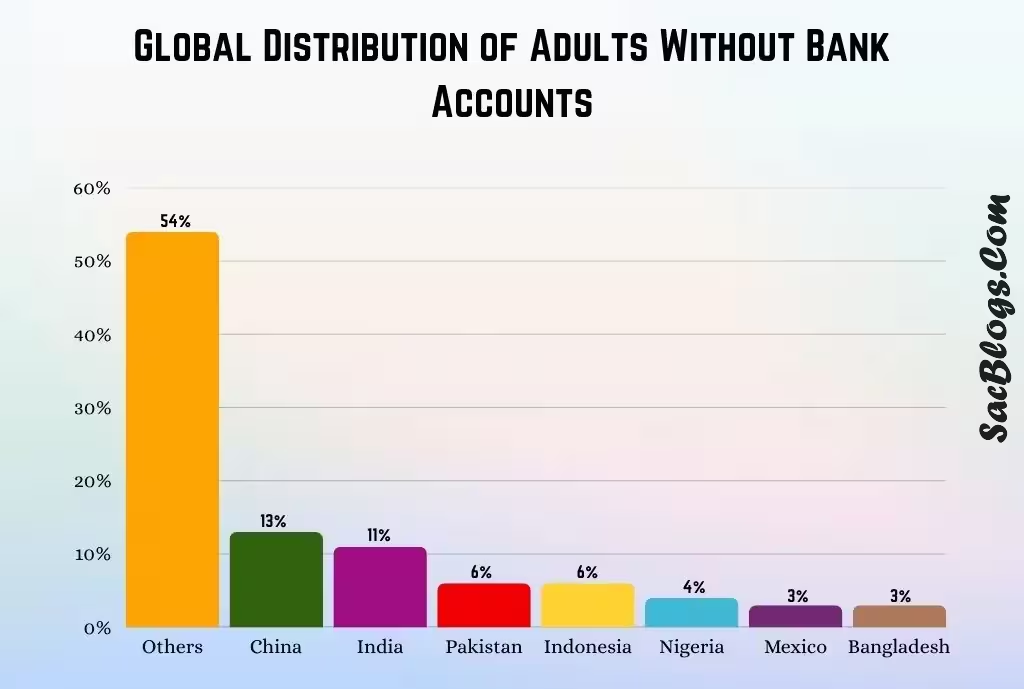

To appreciate the impact of mobile banking and fintech, one must first understand the magnitude of the challenge. Despite a population of 241 million people, only about 21% of Pakistani adults had access to a bank account or mobile money provider until recently . This left a vast portion of the population dependent on informal and often insecure financial networks.

The issue of financial exclusion is not evenly distributed. It disproportionately affects specific demographic groups, creating pockets of deep financial isolation.

- The Rural-Urban Divide: Rural populations face a significant lack of physical banking infrastructure. In 2022, Pakistan had only 10.8 commercial bank branches per 100,000 adults—one of the lowest ratios in the region . This makes accessing a bank a day-long endeavor for many, creating a natural barrier to entry.

- The Gender Gap: Financial exclusion hits women worse than men, who are only half as likely as men to have access to banking services . Cultural barriers and mobility restrictions have historically prevented women from participating in the formal financial system, limiting their economic independence.

- The Impact of Low Income and Education: A lack of formal income and financial literacy are also key barriers. Many of the unbanked work in the informal sector or have irregular income streams, making them feel ineligible for traditional banking services .

The Driving Forces: Catalysts of the Digital Finance Boom

The surge in digital finance is not accidental. It is the result of a powerful convergence of regulatory support, technological adoption, and innovative business models.

Government and Regulatory Push

The State Bank of Pakistan (SBP) has been a central force in driving financial inclusion. Its National Financial Inclusion Strategy has laid the groundwork for a more inclusive financial ecosystem . A landmark decision is the government’s plan to digitize all federal, provincial, and local government payments by June 2026 . This move will not only enhance transparency but also familiarize millions with digital transactions.

Furthermore, the SBP has granted In-Principle Approval (IPA) for establishing five digital retail banks . These banks are specifically tasked with serving segments that conventional banks have neglected, such as SMEs and remote communities.

Technological Infrastructure and Adoption

Widespread mobile phone penetration is the bedrock of this revolution. With over 76% of the population expected to own a mobile device by 2025, the primary tool for accessing financial services is already in people’s hands . This has been complemented by the launch of Raast, Pakistan’s free instant payment system, which simplifies transactions using just a mobile number . By the end of September 2024, daily Raast transactions had reached 3 million, demonstrating rapid adoption .

The Fintech Innovation Ecosystem

Fintech companies have been the agile innovators, filling gaps left by traditional banks. They have leveraged mobile technology to create user-friendly, accessible, and low-cost financial products. The success of platforms like JazzCash and EasyPaisa has shown that a sustainable business model can be built around serving the mass market, including low-income populations .

Key Initiatives Reshaping the Landscape in 2026

Several key initiatives and business models are at the forefront of empowering the unbanked in Pakistan.

The Rise of Digital-Only Banks

The five digital banks approved by the SBP—HugoBank, KT Bank, Mashreq Bank, Raqami Islamic Digital Bank, and Telenor Microfinance Bank—represent a new era of banking . Unlike traditional banks, their model is built for the smartphone era, offering services that are:

- Accessible: No need for physical branches.

- Affordable: Lower operational costs translate to lower fees.

- Customer-Centric: Designed around user-friendly digital experiences.

One of these banks, Mashreq, has reported over 90% operational readiness and expects to start full-fledged operations within months in 2025, setting the stage for a transformed landscape in 2026 .

Leveraging Local Trust: The Agent Network Model

Understanding that a pure digital approach can be intimidating, fintechs have built extensive networks of human agents. These agents, often local shopkeepers, operate as neighborhood banking points. Companies like ZAR are leveraging this model, partnering with “thousands of neighborhood shops, remittance agents, and payment kiosks” to allow users to convert cash into digital currency instantly . This hybrid approach bridges the gap between the familiar cash economy and the new digital one, building trust at a community level.

The Stablecoin Experiment

Looking to the future, Pakistan is exploring the use of blockchain technology and a rupee-backed stablecoin to enhance financial access and streamline remittances . A stablecoin—a digital currency pegged to a stable asset like the rupee or the US dollar—can protect savings from inflation and make cross-border transactions cheaper and faster. ZAR’s mission, for instance, is to use dollar-backed stablecoins to provide financial stability to Pakistan’s unbanked .

Financial Inclusion for Women

Targeted efforts are underway to close the gender gap in financial access. The Asian Development Bank is implementing the Women Inclusive Finance Sector Development Program (WIFSDP). This program supports the State Bank of Pakistan in training and deploying more women branchless banking agents in rural and remote areas, making services more accessible and culturally appropriate for underserved women .

Tangible Impacts: How Digital Finance is Changing Lives

The shift to digital finance is more than a technological upgrade; it is having a concrete impact on the ground.

| Benefit | Manifestation |

|---|---|

| Financial Inclusion | Access to accounts, savings, credit, and insurance without a physical bank branch . |

| Economic Empowerment | Support for small businesses and freelancers through access to capital and digital payment tools. |

| Cost and Time Savings | Dramatic reduction in transaction fees and time spent traveling to and queuing at banks. |

| Increased Transparency | Digital trails reduce corruption and improve the efficiency of government aid distributions. |

- For Individuals and Families: Digital wallets provide a safe place to save money, shielding cash from theft or loss. They also facilitate easier bill payments and domestic money transfers, saving users significant time and money.

- For Small Businesses and the Retail Sector: The robust retail sector, which makes up almost 18% of Pakistan’s GDP, is a major beneficiary . Digital payments reduce the risks and costs of handling cash. Moreover, platforms are now offering working capital loans based on a business’s digital transaction history, providing credit to those who were previously “unscoreable” .

- For the National Economy: The World Bank has emphasized that export-led growth is key to Pakistan’s economic stability . A digitized financial system, including emerging IT service exports, relies on efficient digital payment rails. Furthermore, as more economic activity enters the formal digital sphere, the government’s ability to collect taxes fairly and efficiently improves, strengthening the country’s fiscal position.

Hurdles on the Road to Full Inclusion

Despite the promising progress, several challenges must be overcome to achieve full financial inclusion by 2026.

- Digital Literacy and Mindset: A significant portion of the population lacks the confidence or knowledge to use digital financial services. Convincing people to trust a smartphone with their life savings, especially in an environment where news of cyber theft is prevalent, requires a major shift in mindset .

- Infrastructure and Connectivity: Reliable and affordable internet connectivity remains a challenge, particularly in remote rural areas. Without this foundational infrastructure, digital finance cannot reach its full potential.

- Cybersecurity and Consumer Protection: As the digital footprint expands, so does the risk of cybercrime. Building robust cybersecurity systems and implementing strong consumer protection policies are critical to maintaining public trust . Currently, fewer than half of developing Asian countries have robust data protection laws .

- Interoperability: For a truly efficient ecosystem, different digital payment systems (banks, fintechs, government platforms) need to communicate and transact with each other seamlessly. Ensuring full interoperability is a complex but necessary task.

The Road to 2026 and Beyond: Future Outlook

The trajectory for Pakistan’s digital finance landscape is decidedly positive. The SBP has noted that 83% of financial transactions are already conducted online, though a majority of the value is still transferred via conventional methods . This indicates a strong foundation of user familiarity that digital banks can build upon.

Experts predict that by 2025, over 80% of financial transactions in Pakistan will be digital . The full operationalization of the five digital banks in 2025 will be a key driver for this trend in 2026, offering more choice and innovation. Furthermore, the exploration of advanced technologies like Artificial Intelligence (AI) for fraud detection and blockchain for secure transactions will continue to enhance the security and efficiency of the ecosystem .

The journey is a marathon, not a sprint. As the CEO of Mashreq Bank Pakistan noted, global experience suggests it takes 10 to 15 years to completely shift people from conventional to digital banking . However, the concerted efforts of the government, regulators, and private sector have set Pakistan on an irreversible path toward a more financially inclusive future.

Conclusion

The empowerment of Pakistan’s unbanked population through mobile banking and fintech is one of the most significant economic stories of the decade. By leveraging technology, Pakistan is not just building a more efficient financial system; it is building a more equitable and just society where everyone has the tools to save, invest, and secure a better future. The road to 2026 is filled with both opportunities and obstacles, but the collective commitment to digital financial inclusion promises to unlock the immense potential of millions of Pakistanis, fueling lasting progress and prosperity for the entire nation.

Read Also:

- Why Cashless Payments Are the Future of Business in Pakistan in 2026

- Fintech Innovation in Pakistan – Opportunities, Challenges, and the Road Ahead 2026

- From Cash to Clicks – The Future of Cashless Payments in Pakistan 2026

Frequently Asked Questions (FAQs)

1. What does “unbanked” mean in the context of Pakistan?

In Pakistan, the “unbanked” refers to the millions of adults who lack access to basic formal financial services like a bank account, credit, or insurance. This population often relies on cash and informal networks for their financial transactions, which can be risky and expensive .

2. How are digital banks different from the mobile apps of traditional banks?

Digital banks are licensed banks that operate exclusively online without physical branches, which allows them to offer lower fees and more innovative, mobile-first products. Traditional bank apps are an extension of a brick-and-mortar bank, often still tied to the legacy systems and costs of a physical network .

3. Are digital payments and mobile wallets secure?

Major digital payment platforms in Pakistan implement robust security measures such as encryption, two-factor authentication, and fraud detection systems. While no system is 100% immune, these measures make transactions significantly safer than carrying large amounts of cash .

4. What is being done to help women gain financial access?

Targeted programs like the Women Inclusive Finance Sector Development Program (WIFSDP) are being implemented. These initiatives focus on deploying more women banking agents in rural areas and creating policies that specifically address the cultural and structural barriers women face .

5. Can I use digital banking if I live in a village with a poor internet connection?

Fintech companies are addressing this through hybrid models. You can use a local agent’s kiosk to conduct transactions even with limited personal connectivity. Furthermore, many services offer USSD codes that work on basic feature phones without requiring an internet connection .

6. What is a stablecoin and how could it help Pakistanis?

A stablecoin is a type of digital currency whose value is pegged to a stable asset, like the US dollar or the Pakistani rupee. It could help by providing a safe store of value protected from local currency volatility and by making cross-border remittances faster and much cheaper for overseas Pakistanis sending money home .

7. How is the government encouraging the use of digital payments?

The government is leading by example, mandating the digitization of all government payments by 2026. It is also promoting the use of digital methods for tax payments and pensions, and supporting the development of infrastructure like the Raast instant payment system .

8. What are the biggest challenges facing the growth of fintech in Pakistan?

The key challenges include improving digital literacy, expanding reliable internet infrastructure to remote areas, strengthening cybersecurity measures, and building public trust in digital systems over traditional cash-based transactions .

9. How can small shopkeepers and businesses benefit from this shift?

Small businesses can benefit from faster and safer transactions, better cash flow management, and access to credit based on their digital transaction history. Digital records also make it easier for them to comply with tax regulations and secure loans .

10. What is the future of digital finance in Pakistan beyond 2026?

The future will likely see deeper integration of technologies like AI and blockchain, the potential introduction of a Central Bank Digital Currency (CBDC), and a financial ecosystem that is increasingly personalized, secure, and accessible to every citizen, ultimately making financial exclusion a thing of the past .

2 thoughts on “How Mobile Banking and Fintech Are Empowering the Unbanked in Pakistan for 2026”